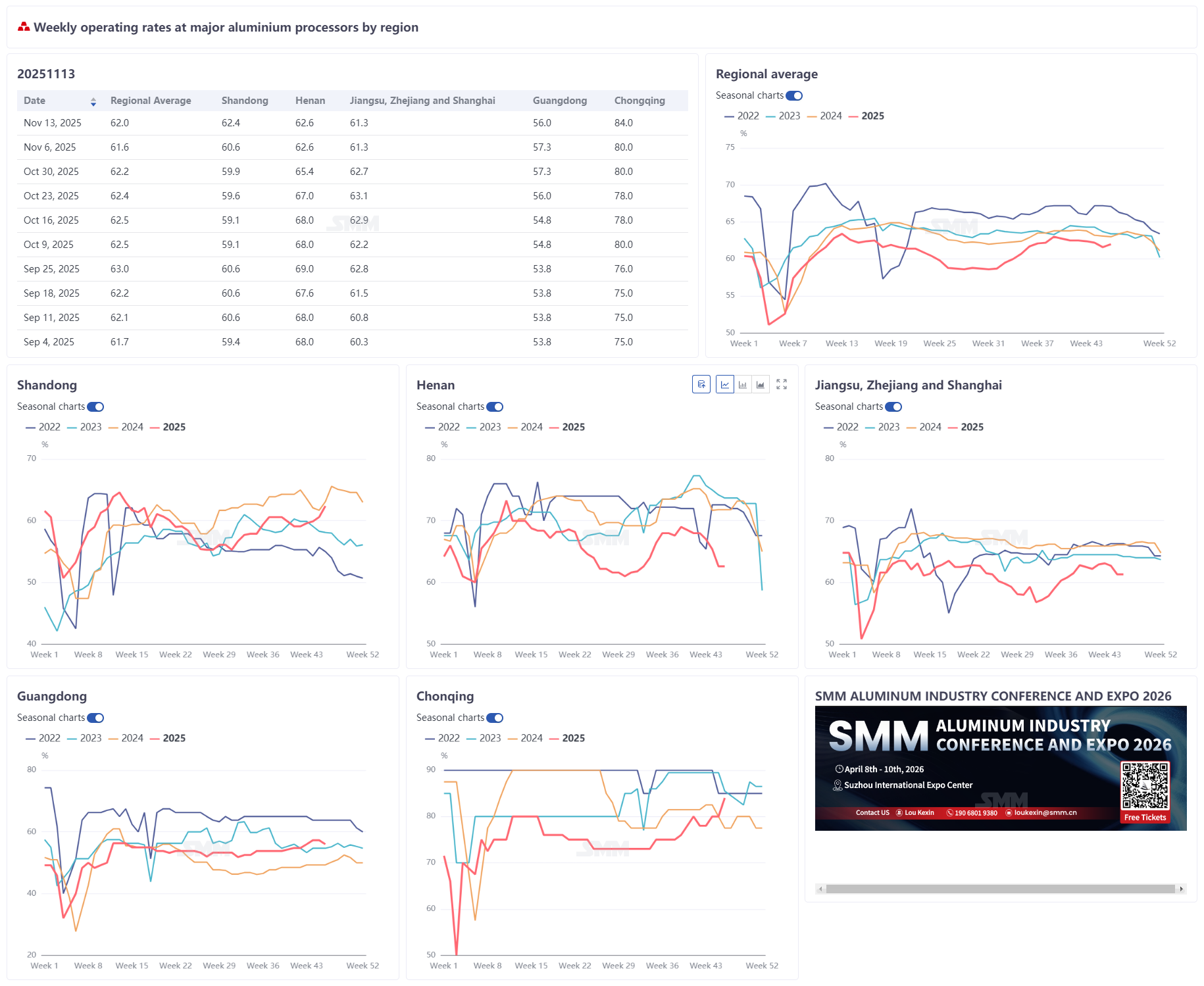

November 14, 2025:

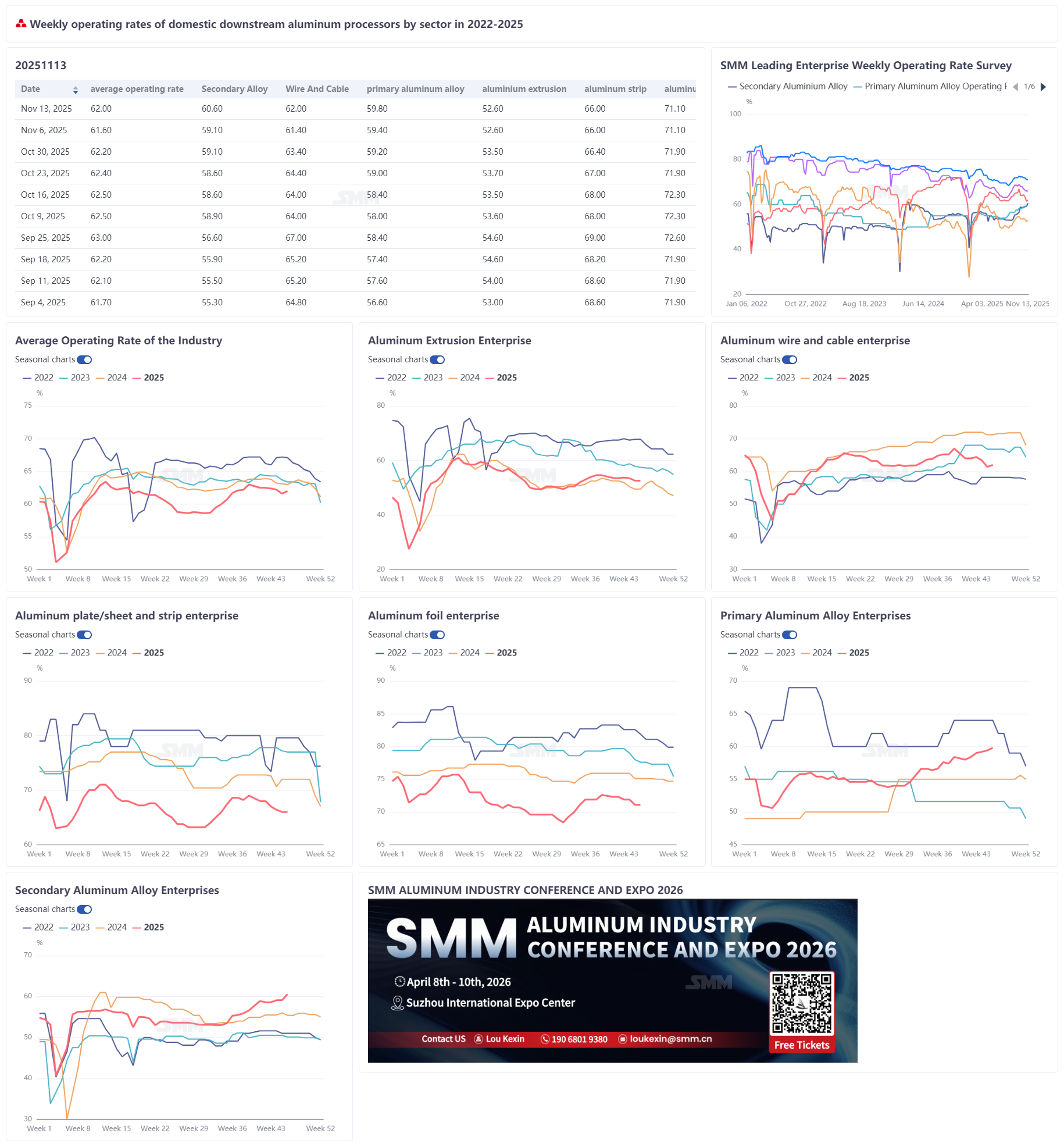

This week, the overall operating rate of leading downstream aluminum processing enterprises in China rose slightly by 0.4 percentage points WoW to 62%, showing a structurally divergent trend across the market. By segment: the operating rate for primary aluminum alloy increased by 0.4 percentage points to 59.8%, as mainstream producers maintained stable production schedules, downstream manufacturing orders grew YoY, and the market remained in the peak season; the operating rate for aluminum wire and cable edged up 0.6 percentage points to 62%, supported by the fulfillment of orders from State Grid and China Southern Power Grid, though capacity utilization stayed low with insufficient order saturation; the operating rate for aluminum extrusion held flat WoW at 52.6%, with automotive and PV extrusions performing steadily while construction extrusions remained sluggish, and high aluminum prices sparking concerns about "steel replacing aluminum"; the operating rate for aluminum plate/sheet and strip remained at 66.0%, with demand from new energy-related sectors supporting full-load operation on some production lines, but environmental protection-related controls and weak off-season demand kept overall performance under pressure; the operating rate for aluminum foil held at 71.1%, with strong orders for new energy-related products like battery foil, but demand for double zero foil, decorative foil, and export packaging foil weakened; the operating rate for secondary aluminum producers increased by 1.5 percentage points to 60.6%, driven by order growth at large sample enterprises, yet tight aluminum scrap supply and persistent losses constrained capacity release across the sector. SMM expects the operating rates in the downstream aluminum processing industry to show a diverging trend in the short term, with aluminum wire and cable supported by grid orders to continue a slight rebound, while aluminum plate/sheet and strip and aluminum foil are likely to gradually decline due to recurring environmental controls and off-season effects.

Primary Aluminum Alloy: The primary aluminum alloy industry continued stable operation this week, with the operating rate rising slightly by 0.4 percentage points to 59.8%. Supply side, mainstream enterprises maintained steady production schedules, unaffected by aluminum price fluctuations, with overall production levels continuing to climb and the industry's supply landscape steadily improving. Demand side, downstream manufacturing orders increased from previous levels, driving synchronous growth in demand for primary alloy. Some enterprises reported current orders were higher than before, the operating rate continued to rise, and the growth rate accelerated further WoW. The industry overall remains in the peak season, performing better than the same period last year. The operating rate is expected to maintain a slow upward trend going forward.

Aluminum Plate/Sheet and Strip: The operating rate of leading aluminum plate/sheet and strip enterprises was 66.0% this week. In central China, recurring smog led to ongoing environmental protection inspections without signs of easing, putting significant pressure on local producers' operations. Aluminum prices quickly rising above 22,000 yuan/mt this week triggered wait-and-see sentiment among downstream buyers, reducing cargo pick-up enthusiasm. Some enterprises initiated new rounds of processing fee discounts to reduce inventory, reinforcing expectations of weakening demand. Industry orders showed structural differences. By mid-November, demand support from new energy-related sectors like automotive sheet, battery shells, and brazing materials kept production lines at full capacity, but this was insufficient to offset declines in sectors like construction and packaging. Looking ahead to next week, ongoing environmental protection disruptions in Henan, coupled with weak off-season demand, are expected to lead to a continued contraction in the operating rate for the aluminum plate/sheet and strip industry, with the medium and long-term downward trend difficult to reverse.

Aluminum Wire and Cable: The weekly operating rate for aluminum wire and cable increased slightly by 0.6 percentage points WoW to 62% this week, showing recovery after last week's decline caused by regional environmental protection-driven production restrictions. The slight rebound was primarily due to State Grid placing overhead line orders this week, coupled with some China Southern Power Grid orders entering the matching phase. Orders from these two major grid operators provided direct support for enterprise production, leading to a slight recovery in operating load. From an operational perspective, although the operating level improved WoW, current capacity utilization remains relatively low, not exiting the low-range operation zone, with production still in a mild recovery state. Regarding industry order dynamics, the continuity of State Grid order tenders and new matching orders from China Southern Power Grid combined to effectively offset the impact of previous weak end-use demand, becoming key drivers supporting the operating rate recovery. Looking ahead to next week, benefiting from continued grid order support, the aluminum wire and cable operating rate is expected to maintain a slight rebound. However, constrained by overall low capacity utilization, significant upward momentum is lacking, and the rate will likely fluctuate rangebound between 62%-63% next week.

Aluminum Extrusion: The weekly operating rate for the domestic aluminum extrusion industry was 52.6% this week, unchanged WoW. Recently, aluminum prices have remained high, fostering strong wait-and-see sentiment in the downstream market. Extrusion enterprises generally maintain orders on hand covering about 7 to 10 days, with some better-performing enterprises having orders covering around one month. Despite price pressures, consumption showed some resilience; current operating performance did not show the significant decline previously anticipated by the market. By segment, construction extrusions overall remain sluggish. For industrial extrusions, automotive extrusion is still the relatively better-performing area. However, according to feedback from an enterprise in north-east China, its partner automaker is researching using steel parts to replace aluminum parts. Although such steel parts weigh nearly twice as much as aluminum parts, their cost is only one-third. The enterprise is concerned that persistently high aluminum prices could accelerate the substitution process of "steel replacing aluminum". PV extrusion operations remained generally stable. An enterprise in Anhui indicated that, having concentrated on completing a batch of orders in the first half of the month, its current operating rate basically maintained the level from the end of last month. SMM will continue monitoring order changes across various segments.

Aluminum Foil: The operating rate of leading aluminum foil enterprises was 71.1% this week. At the operational level, environmental protection-related controls in Henan forced some aluminum foil producers to adjust production plans. Although leading enterprises did not cut production, high aluminum prices dampened downstream order placement enthusiasm, leading to issues like high inventory and capital tie-up. Industry orders showed significant divergence: demand for battery foil and brazing foil remained robust, with orders fully booked for domestic Q3 and Q4 causing some enterprises to shift packaging foil capacity to battery foil production; orders for double zero foil and decorative foil weakened, and export stockpiling for packaging foil neared its end as concentrated overseas stockpiling in September-October was completed, with export support gradually weakening. Looking ahead to next week, as the off-season deepens, risks of weakening end-use demand persist, and the operating rate for leading aluminum foil enterprises is expected to gradually decline.

Secondary Aluminum: The operating rate of leading secondary aluminum enterprises increased by 1.5 percentage points WoW to 60.6% this week, mainly driven by order growth at large sample enterprises. However, capacity release in the sector still faces multiple constraints: persistent pressure on the raw material side: the tight supply pattern for aluminum scrap remained unchanged, with prices rising in tandem with aluminum prices, exacerbating cost pressure for secondary aluminum alloy producers and deepening industry losses; rapid aluminum price increases suppressed demand: although end-use demand was stable with a slight increase, aluminum prices soaring to the high of 22,000 yuan/mt intensified market fear of high prices. Some die-casting plants became more cautious in procurement, enterprises with sufficient inventory focused on digesting existing stock, procurement pace slowed, while low-inventory enterprises only maintained rigid procurement. Reduced new orders at alloy plants constrained upside room for the operating rate. In the short term, the operating rate of leading enterprises is expected to be mainly stable with a slight increase, depending on the improvement in aluminum scrap supply and changes in procurement pace of downstream enterprises under high prices.

![Aluminum Producers' Operating Rates Rebound to 61.9%; High Prices Challenge "Golden March" Peak Season [SMM Survey]](https://imgqn.smm.cn/usercenter/tXCfs20251217171653.jpg)

![ADC12 Prices Rose Again This Week[[Weekly Review of Aluminum Scrap and Secondary Aluminum]]](https://imgqn.smm.cn/production/admin/votes/imageskkgTu20240508153005.png)